Taking the first step to turn an idea into a business or to practice a profession independently in Chile involves a fundamental procedure: the Start of Activities before the Internal Revenue Service (SII). This process is the gateway to the formal business world and is crucial to operate within the legal framework.

Below, we break down everything you need to know about this important procedure.

What is the Start of Activities?

El Inicio de Actividades es una declaración jurada formal que una persona natural o jurídica (empresa), realiza ante el SII para informar que comenzará a desarrollar actividades económicas que pueden generar rentas y, por lo tanto, estarán sujetas al pago de impuestos.

In simple terms, it's like «raising your hand» and telling the SII: «Hello! I'm going to start generating income and I want to do it legally».

This procedure assigns you tax obligations, but it also grants you rights, such as the ability to issue essential tax documents:

- Fees Receipts: If you are an independent professional.

- Invoices and Sales Receipts: If you have a company or sell products/services.

Carrying out the Start of Activities is the starting point so you can invoice your clients, keep orderly accounting, and meet your tax responsibilities.

What is the legal context of this procedure? (Legal framework)

El marco legal en el cual se basa el Inicio de Actividades ante el SII, no es una sola ley, sino un conjunto normativo que conecta la existencia de una actividad económica con las obligaciones tributarias correspondientes.

The most important aspects are:

1. Fundamental Pillar: The Tax Code: It is the main rule that establishes the obligation to start activities, in its Decree Law No. 830. This legal body is the backbone of the Chilean tax system.

- Article 68° of the Tax Code: It is the key and most important article. It explicitly establishes the obligation, within a two-month period.

- Article 97° No. 1 of the Tax Code: It establishes the sanctions for not complying with this obligation. It is sanctioned with a fine that ranges from 1 UTM (Monthly Tax Unit) to 1 UTA (Annual Tax Unit).

2. Specific Tax Laws: Once activities are started, the taxpayer is subject to specific taxes. The two most relevant laws are:

- Decree Law No. 824 – Income Tax Law (LIR): Define qué se considera «renta» y, por lo tanto, qué tipo de actividades están obligadas a inscribirse en el SII. Este trámite te clasifica como contribuyente de Primera o Segunda Categoría, dependiendo de la naturaleza de tus ingresos.

- Decree Law No. 825 – Law on Sales and Services Tax (VAT Law): It regulates the Value Added Tax (VAT) and other taxes specific to consumption.

3. Resolutions and Circulars of the SII: The SII, in its role as administrator and auditor, issues its own regulations to instruct on the practical application of the laws.

These resolutions and circulars establish the «step by step» of the process, the forms, the deadlines, and the specific requirements.

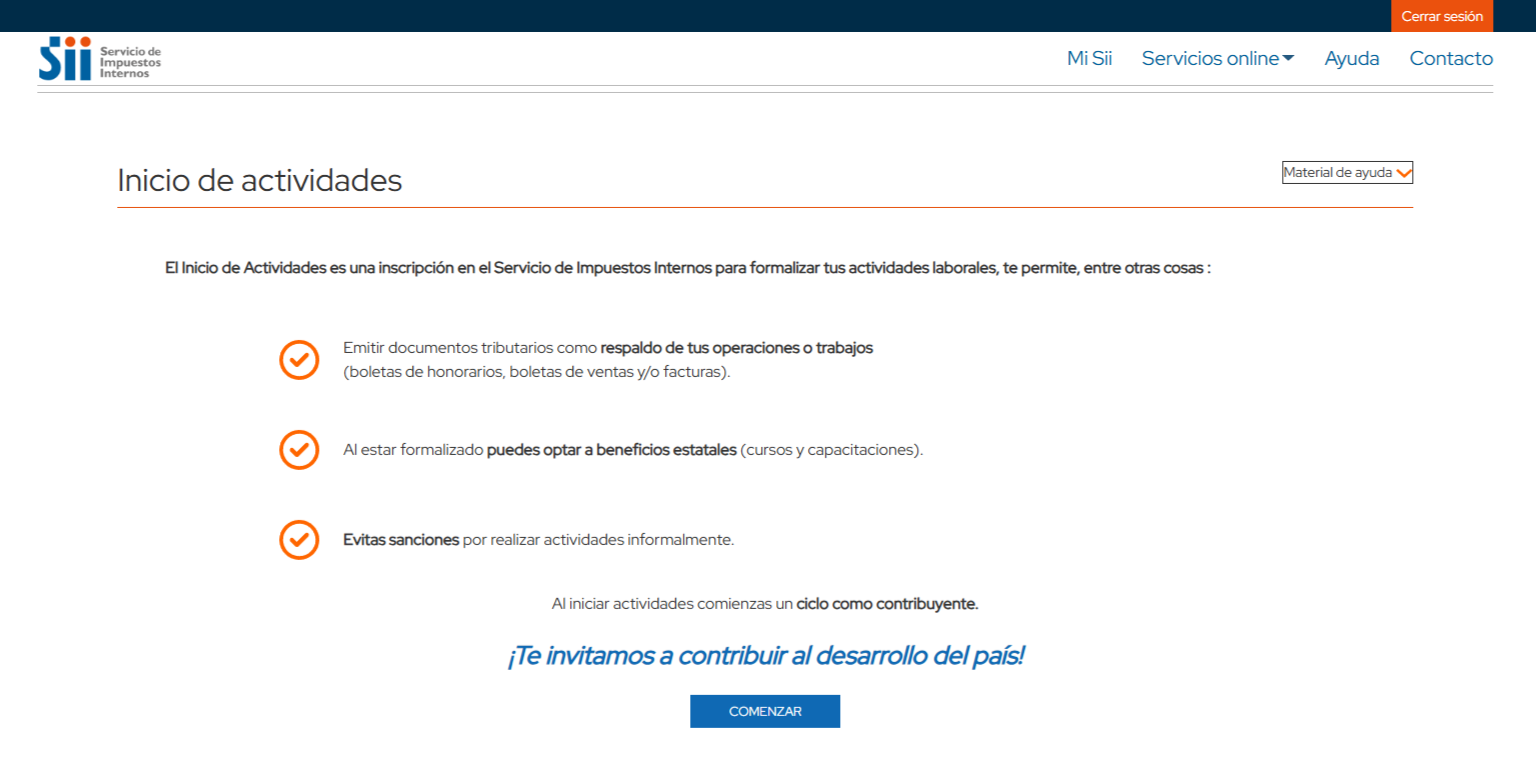

How is the Start of Activities carried out?

Afortunadamente, hoy en día este proceso se puede realizar de manera 100% online a través del portal del SII, lo que lo hace más rápido y accesible. Es importante tener en cuenta que se debe ingresar desde el usuario del Legal Representative of the company. The general steps are as follows:

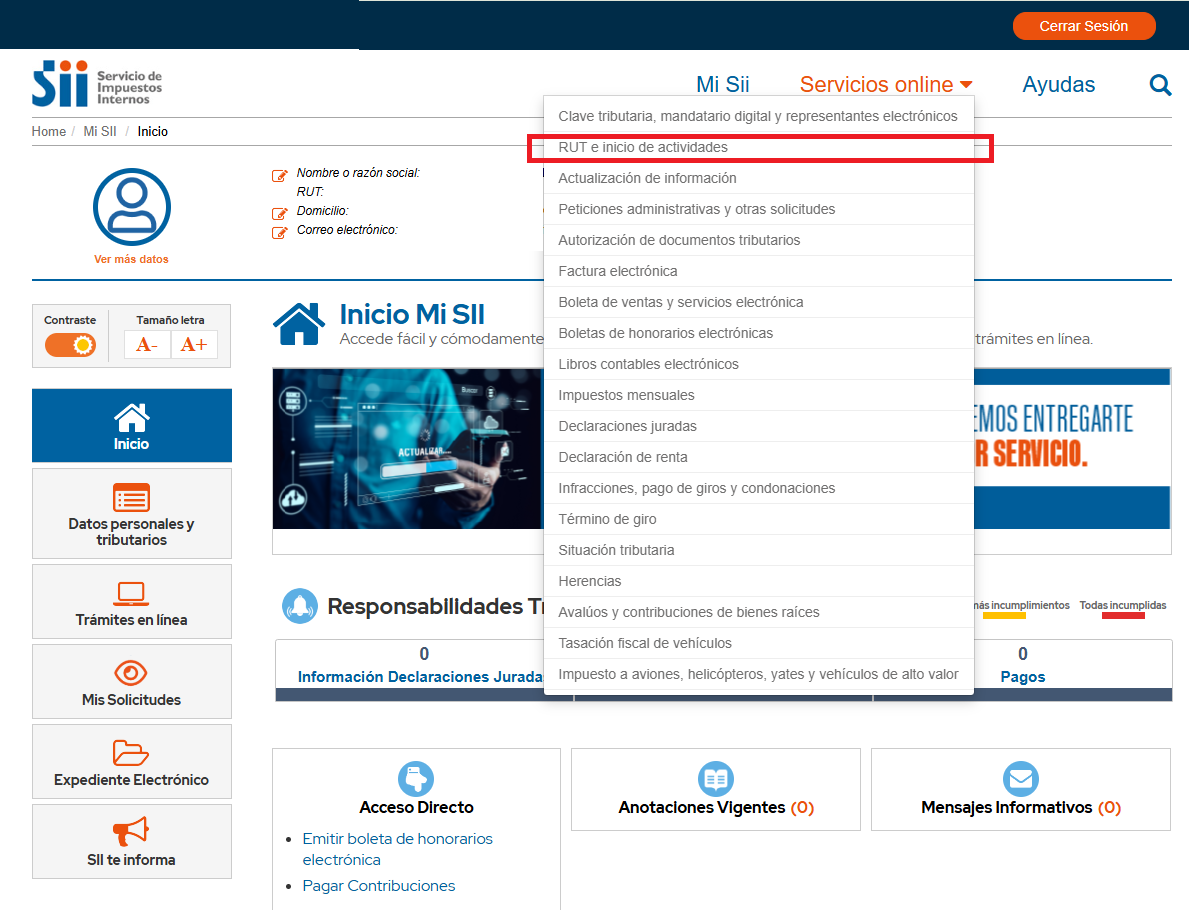

Step 1: Enter the SII portal and select the “Start of Activities” option

- Enter www.sii.cl.

- Go to the «Online Services» section.

- Select «RUT and Start of Activities».

- Click the «Start of Activities» option.

Step 2: Complete the electronic form

The system will guide you to fill out the digital form. The key information you must provide is:

- Identification: Your RUT (if you are a natural person) or the company’s RUT.

- Initial capital: The amount, in money or assets, with which you will start your business. It must be a reasonable and justifiable figure.

- Tax domicile: The address where you will carry out your activity or the one you will register for SII notification purposes. You must prove this domicile.

- Economic activities: You must describe what you will do, using Economic Activity Codes, which you will select from a list. It is crucial to choose the correct codes, as they will define your tax obligations.

- Tax Regime: Deberás elegir un régimen para el pago de tus impuestos. Esta es una decisión muy importante, por lo que se recomienda contar con la asesoría de un contador para elegir el más conveniente para tu modelo de negocio.

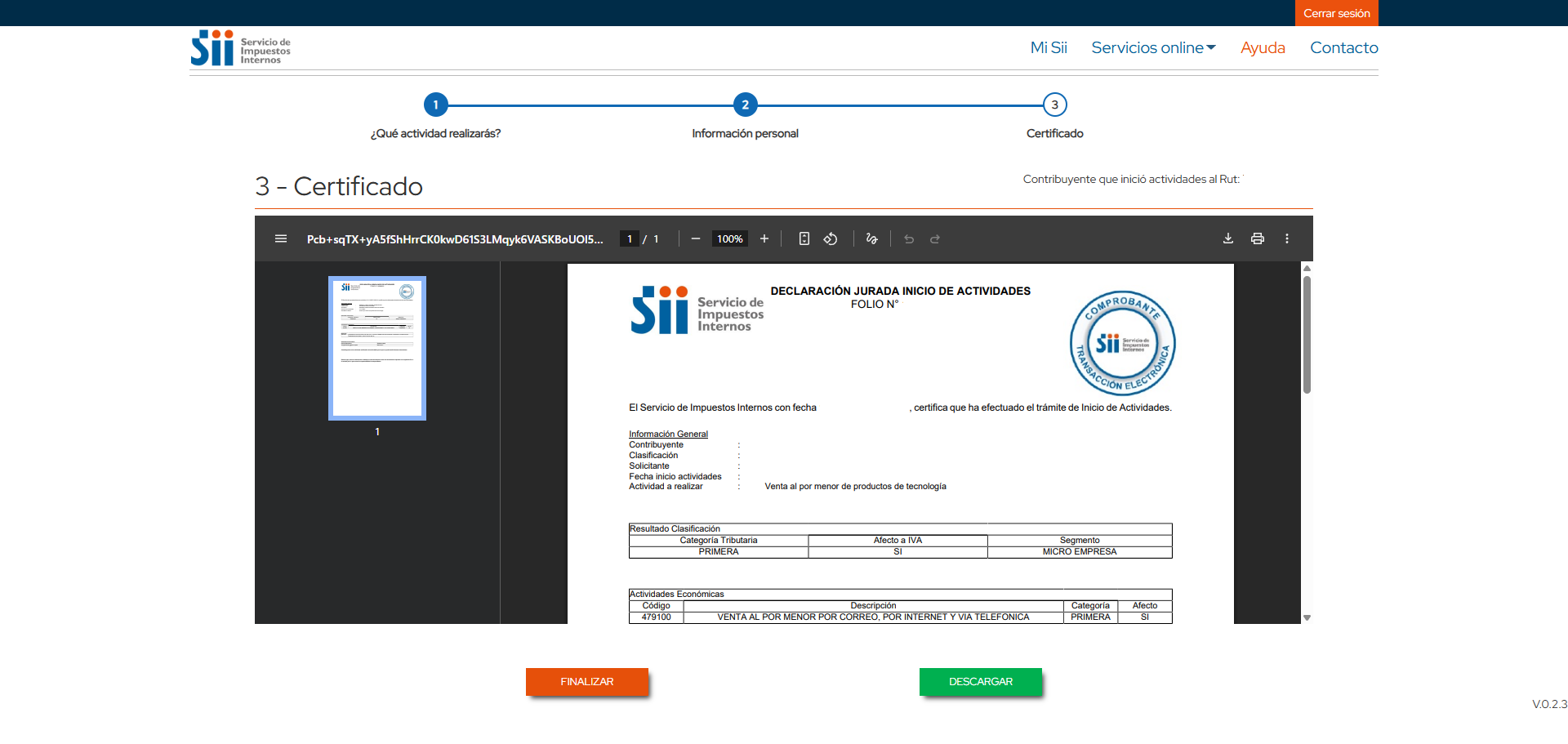

Step 3: Confirmation of the information provided

Once all the information is entered, the system will ask you to validate the procedure, thus issuing a Sworn Statement of Commencement of Activities document

What are the fundamental requirements?

The requirements vary slightly depending on whether you are a natural person or a legal entity.

For Natural Persons (professionals, trades):

- Be over 18 years old.

- Have a valid Chilean Identity Card.

- Have no tax impediments (e.g., serious negative notes in the SII).

- Have a Clave Única or Tax Key.

- Be able to prove an address.

For Legal Entities (Companies: SpA, Ltda., EIRL, etc.):

- Have legally incorporated the company (through the «Tu Empresa en un Día» portal or by the traditional method with a lawyer and notary).

- The company must have a RUT assigned by the SII.

- The legal representative must have a valid Identity Card and Clave Única/Tax Key.

- Be able to prove the company address.

- The deed of incorporation of the company.

What happens if I do NOT carry out the Commencement of Activities?

Operating without having carried out the Commencement of Activities places you in informality and entails serious negative consequences:

- Inability to issue invoices:

No podrás emitir facturas ni boletas de honorarios. Esto te cierra las puertas a clientes que sean empresas, ya que necesitan estos documentos para justificar sus gastos. Limita tu crecimiento a ventas menores e informales.

- Risk of sanctions and fines:

If the SII detects that you are carrying out commercial activities without having formalized your situation, you are exposed to:

- Fines: Penalties range from 1 UTM to 1 UTA (Unidad Tributaria Anual), depending on the severity and duration of the infraction.

- Retroactive Tax Collection: The SII can calculate the taxes you should have paid since you started your activity, applying interest and adjustments. This can result in a considerable debt.

- Closure: In serious and repeated cases, the SII has the authority to close your establishment.

- Lack of access to benefits:

By being informal, you cannot access:

- Bank loans for businesses.

- State funds and subsidies.

- Tax benefits for SMEs.

- Public or private tenders.

- Legal and Commercial Lack of Protection:

Operating informally leaves you without support. You do not have a legal structure that protects your personal assets (in the case of companies), and your professional reputation is diminished.

Start your Inicio de Actividades now

El Inicio de Actividades no es solo un trámite burocrático; es el acto de nacimiento oficial de tu negocio o carrera independiente. Es el pilar sobre el cual construirás un proyecto sólido, legal y con potencial de crecimiento.

Although it may seem like a complex step, the benefits of formality far outweigh the risks and limitations of operating in the shadows.

Si tienes dudas, especialmente en la elección de los códigos de actividad y el régimen tributario, no dudes en buscar asesoría especializada. Esta pequeña inversión inicial te ahorrará muchos problemas y dinero en el futuro.

Make the birth of your company official and legal!

At Iberocapital we help you with the Inicio de Actividades process at the SII without complications, so you can register your company and issue your first invoice in Chile. Contact us now!

Reviews

There are no reviews yet.